Summary

- For Wayfair valuation does matter and it looks significantly overvalued at current levels.

- I hold serious doubts regarding Wayfair in the post-vaccine world with increasing competitive pressures.

- Those looking for an entry should wait for a significant pull-back.

Wayfair (W) has been one of the biggest Covid-19 winners. Shares now stand up 765% from the lows that were experienced at the end of March. Whilst I still favor most tech and e-commerce over the long term, I have doubts regarding Wayfairs immediate potential following a vaccine. I also believe from a technical standpoint Wayfair has further to fall and those investors looking to take a stake for the long run should hold out and wait for a better entry price.

Covid-19

There is no denying Wayfair's exceptionally strong performance through this pandemic as the site has benefited massively from broader online shift of consumer spending and is positioned well for the long term in many ways. So it's only right for me to highlight many of the strong metrics that Wayfair has delivered.

In the most recent quarter, Wayfair delivered earnings of $2.30 per share (non-GAAP) and $1.67 on a GAAP basis, significantly beating the consensus of $0.80 (non-GAAP) while revenue only just beat the consensus of $3.7 billion by $0.1 billion (delivered $3.8 billion in revenues). Another real positive is that Wayfair's number of active buyers remained very strong at 28.8 million, up 50.9% from the prior year. With these strong Q3 results it wasn't of much surprise to see Wayfair surge 15% following the release of these results as the market bought into the continued strong traction that Wayfair was receiving.

It's clear that the market is charging Wayfair with a significant premium because of their strong foothold in the e-commerce furniture and home goods market, which is deemed the future and rightly so. However, the price charged for this future growth is unbelievable for a company that has only just turned a corner in terms of profitability. It appears investors have completely forgotten about the old Wayfair - the one prior to Covid.

Valuation

Yes, Wayfair has turned a corner due to Covid, which has significantly increased its long term viability. In fact, I'd say I believe far more in the effect the pandemic has had on the viability of tech stocks than the average investor. But for me even when considering this, Wayfair is not attractive at current levels. Purely looking at Wayfair on a historic basis, the company has delivered a non-GAAP EPS of just $0.33 over the last four quarters combined. I believe this truly reflects the swing in performance that Wayfair has experienced as a result of the pandemic. It also shows the poor performance Wayfair was actually experiencing prior to the pandemic - losing a significant portion of money. Wayfair has shown strong earnings power with its scale-up revenues and the fact that has expanded margins, but I question Wayfair's ability to do this without broader market headwinds.

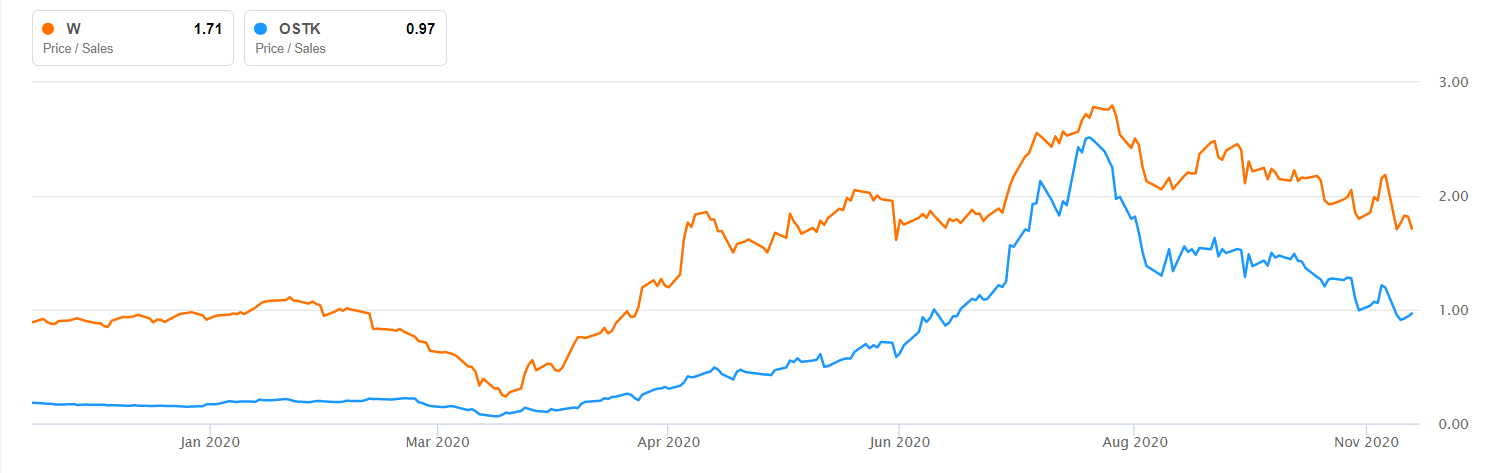

In fact, Wayfair has quite a rocky history looking back at previous quarterly earnings. The company has missed on EPS eight out of the last twelve quarters. Looking at Wayfair's price-to-sales ratio, it comes in at 1.71 which is still significantly higher than the pre-pandemic level of around 1. Comparing that to competitors such as Overstock (OSTK) who have also experienced a large run-up due to the pandemic, Wayfair is still charging a sizable premium comparatively.

Source: Seeking Alpha charting tool

Wayfair's valuation currently implies that there will be a sustained significant shift in consumers to online furniture shopping and that the company will dominate this market. I simply do not believe this is true and that going forward Wayfair will face increased competition, particularly regarding delivery times which is a huge lure for many consumers when ordering bulk items such as furniture. Comparing Wayfair to its P/S in the 2017-19 period the figure actually stands at similar levels to now which might suggest that Wayfair's shares have grown inline with its revenue growth. But once again I question the sustainability of Wayfair's current financials and whether many of the customers who have shopped with Wayfair recently will become repeat buyers once more physical shopping becomes more viable again. I have tabled below the P/S ratios below which were the very rough averages for each year since 2016: