Summary

- Recent advancements in readouts for Xpovio and Selinexor have yet to be reflected in market pricing, in our view.

- Karyopharm has had an in line quarter, where Xpovio sales were driven by new prescriber accounts and upward trends in average refill rate.

- Based on the commercial potential for the Xpovio label and Selinexor as a molecule, we see high upside potential and a fair value range of $33-$41 on today's trading.

- There are concentration risks as a single-molecule pipeline, plus downward pressure on shares YTD presenting pricing risks in the near-term, that must be considered.

- Our outlook is bullish on the company, and we believe investors will begin to reward the company as further data is compiled in their segments over the coming year.

Thesis Summary

We believe the market may be overseeing the value in Karyopharm Therapeutics (NASDAQ:KPTI), particularly on the back of positive top-line results in their phase 3 Boston study, and other advancements. Furthermore, the company has also provided positive data from the phase 3 Seal study, which investigated Selinexor's application to advanced unresectable dedifferentiated liposarcoma and chemo refractory liposarcoma. We believe that KPTI's methodology has helped de-risked towards solid tumor applications, and therefore we hold a positive outlook for Xpovio and Selinexor's next progressions, especially the latter, into earlier treatment lines for multiple myeloma.

Furthermore, based on discussions with experts, we believe Xpovio has additional commercial potential outside of myeloma into life management, with opportunities in select solid tumor and diffuse large B-cell lymphoma. With these facts, together with results from the 3rd quarter, we believe that the current share price doesn't reflect the inherent value in these segments for KPTI, and that there is an asymmetry in risk/reward that is in favor of the upside at this time.

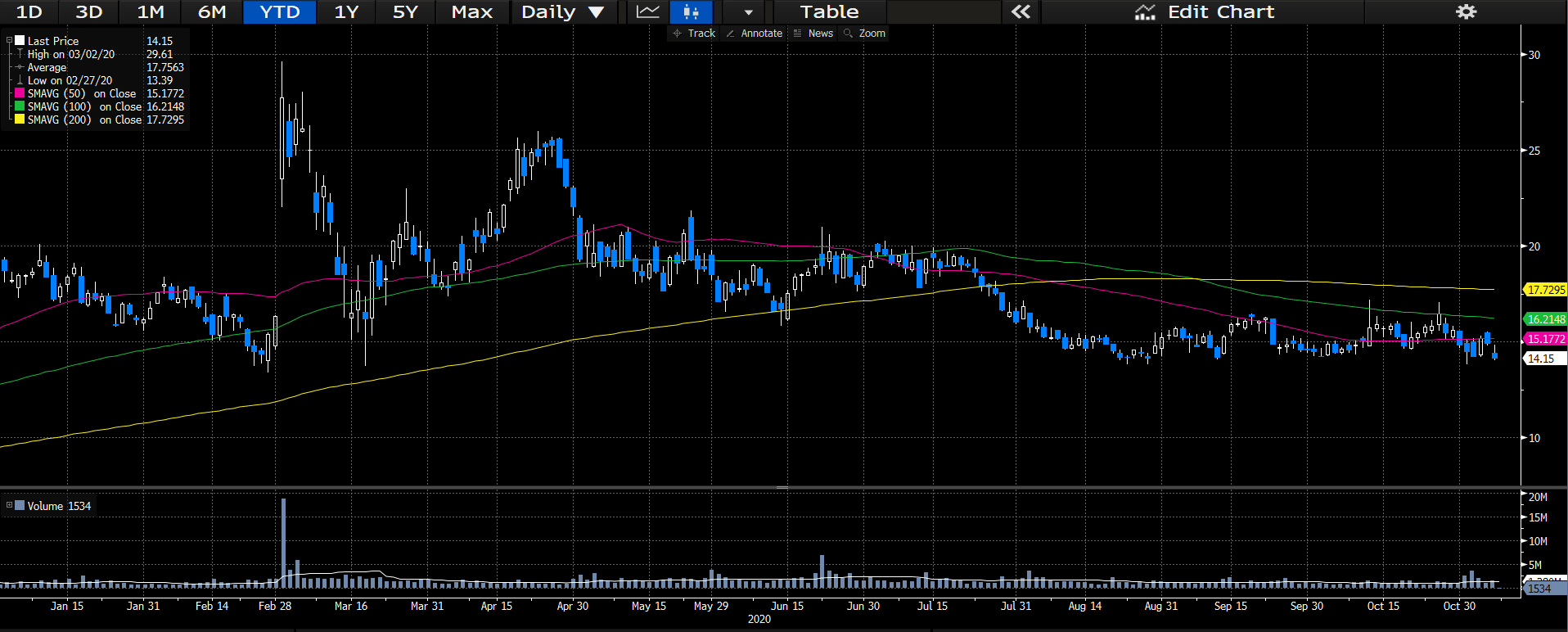

Data Source: Author's Bloomberg Terminal

Catalysts for Long-Term Price Change

KPTI released encouraging top-line data from both phase 3 Boston and Seal studies most recently. The arrival of the data is certainly a catalyst to upside in our view, and the success here has been highlighted as a de-risking for a breadth of solid tumor applications. Whilst the epidemiology and total case rates for advanced unresectable dedifferentiated liposarcoma remain low, we expect upcoming readouts in key trials to add steam and drive share price north over the coming periods. Firstly, there is the updated phase 3 Siendo readouts due next year, which is obtaining evidence of efficacy in Selinexor for patients with advanced and/or recurrent endometrial cancer. This represents the biggest catalyst in the medium-term, in our view. We firmly believe that investors will reward KPTI on the back of positive outcomes from this data. Additionally, the 400 patient phase 2 KING study, that is evaluating oral Selinexor in combination with standard of care therapy in patients with recurrent glioblastoma, will increase investor attractiveness if the readouts show positive results. This is in addition to the combination phase 1 SPRINT study that is now underway, investigating the bioequivalence, tolerability and anti-tumor activity of a Selinexor combination treatment.