Summary

- Bristol-Myers Squibb has finally completed the acquisition of Celgene, now is the time to shine.

- The company performed incredibly well in 2019 - better than it originally anticipated - especially with asset spin-offs. That is expected to continue into the 2020s.

- The company has a significant number of growth opportunities which should be sufficient to prevent it from patent expiration of current drugs.

- The company should be able to generate significant FCF, which as we can see from now until year-end 2023 will enable to repurchase 22% of shares and increase dividends by 10% annually.

- I recommend investing now and holding onto the stock for the long run.

- Looking for a helping hand in the market? Members of The Energy Forum get exclusive ideas and guidance to navigate any climate. Get started today »

Bristol-Myers Squibb (NYSE:BMY) has had a hectic 2019. However, the company has finally closed on its acquisition of Celgene, it has strong long-term prospects to diversify its revenue, and significant cash flow abilities. I believe that these things will allow the company to generate massive rewards for shareholders over the 2020s.

Bristol-Myers Squibb - Wikipedia

Bristol-Myers Squibb 2019 Results

Bristol-Myers Squibb generated strong results in 2019 that support the rationale behind the acquisition and justify the combination behind the behemoths. Traditionally, such a large acquisition does not work out, however, Bristol-Myers Squibb seems to accomplish the unlikely.

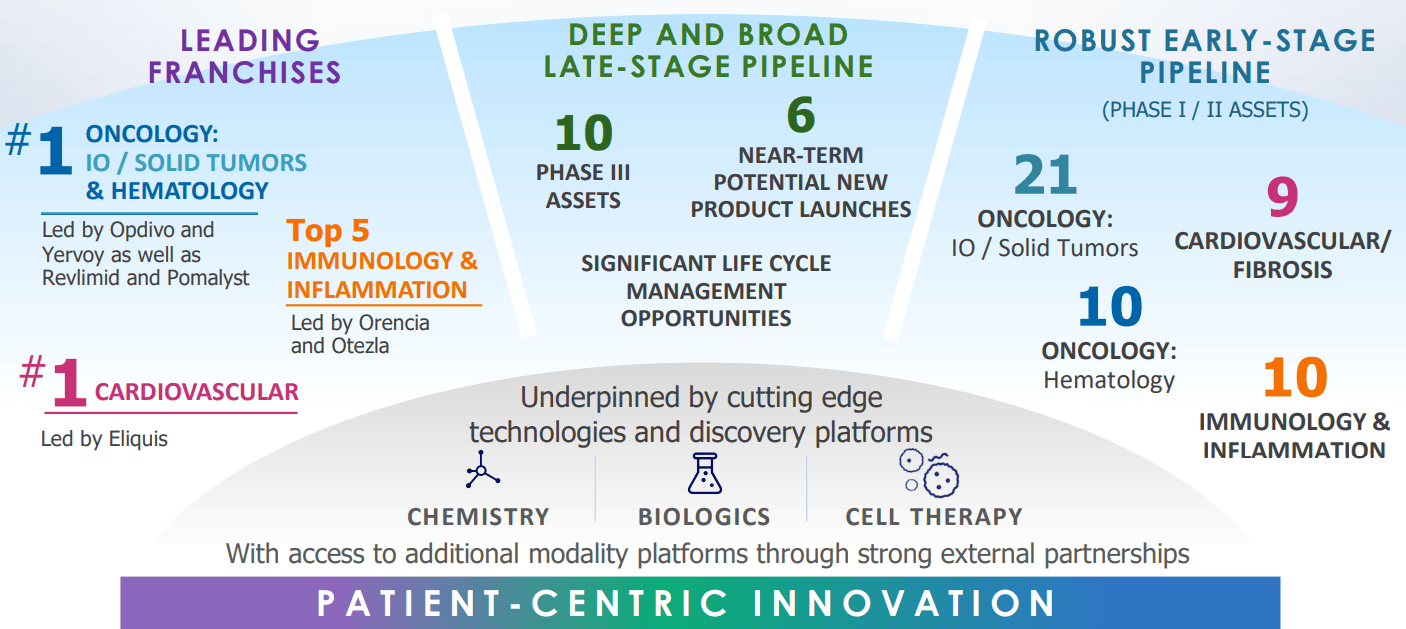

Bristol-Myers Squibb Acquisition Pipeline - Bristol-Myers Squibb Investor Presentation

The above image shows Bristol-Myers Squibb's original rationale behind the acquisition. The combined company would have the #1 largest oncology and cardiovascular franchise along with top 5 immunology and inflammation franchises. At the same time, the company has a deep and broad late-stage pipeline that will result in additional opportunities in the future.

Past all of this, the company has an incredibly strong early-stage pipeline with a number of opportunities. These are supportive of the company's long-term revenue and cash flow potential.

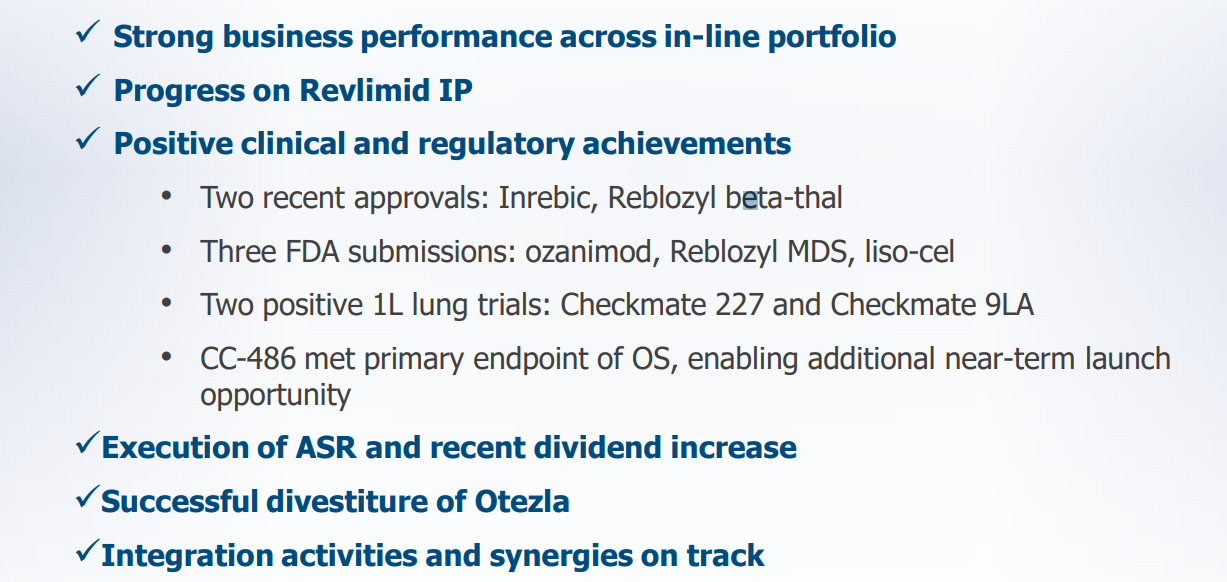

Bristol-Myers Squibb Acquisition Performance - Bristol-Myers Squibb Investor Presentation

Since the acquisition, the company has had strong performance across its portfolio and made significant progress on its Revlimid intellectual property. For perspective, Revlimid was Celgene's most important and best known drug and incredibly important to the combined company.

At the same time, the company has had a number of major clinical and regulatory achievements. This has resulted in the BMY.RT ADR that was based on drug approvals of Celgene's major assets (worth up to $9 / share) increasing in value by 75% since it was first publicly traded. That's the market showing the potential of this and it's one more way Celgene shareholders are rewarded.

{kind=link}