Summary

- The company's share price has crashed, first on disappointing Q3 figures, then on the proposed acquisition of ECI.

- We think the selloff on the Q3 figures is not really justified, and have made the shares quite cheap.

- However, their proposed acquisition of ECI is a risky bet. The rationale for the acquisition is clear, but the financial foundation leaves little room for error, in our view.

It has not been a good year for Ribbon Communications (RBBN) with the shares down 35.7% last year:

After being range bound for most of the year, the crash happened in two installments:

- End of October on the Q3 results

- Mid November on the proposed acquisition of privately held ECI

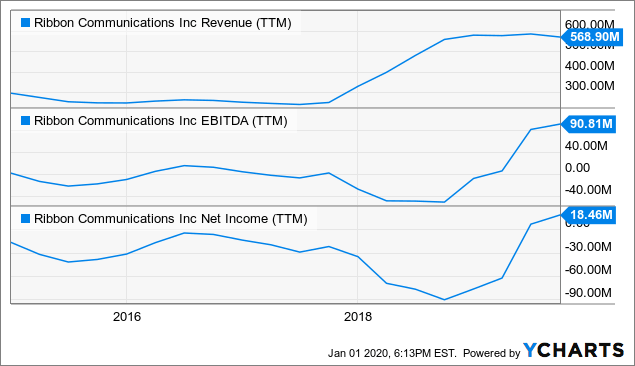

At first sight, the share price crash looks rather curious as there is a lot of improvement, both in revenues and operational metrics:

Data by YCharts

Data by YChartsThese are mostly the result of acquisitions (which are, of course, responsible for the marked deterioration in the GAAP income and EBITDA figures in 2018):

- Edgewater Networks (for $110M), which closed on August 3, 2018.

- Anova Data, which closed on n February 28, 2019.

The company seems to have digested these acquisitions quite well (although Anova is small, Edgewater is quite substantial, producing $64M revenue in 2017), something to keep in mind.

Q3 results

The Q3 results were disappointing, with both revenue (at $138M missing by $18.6M) and non-GAAP EPS (coming in at $0.13 where $0.20 was expected) to blame.

However, not all was bad news, in fact both gross margin as well as operating margin actually increased, so the disappointing profit performance is entirely the result of the revenue shortfall, from the earnings deck: