Summary

- Akamai has one of the world’s largest CDN configurations of servers and networks.

- Akamai appears to be treading water with an eroding business instead of aggressively growing its TAM.

- The stock is overvalued, and with expected revenue growth rate of 8%, it is an unexciting investment.

- I have assigned Akamai a neutral rating.

Akamai Technologies, Inc. (AKAM) is a Content Delivery Network (CDN) provider with one of the world’s largest configurations consisting of 240,000 servers, 1,700 networks, 3,900 locations in 133 countries, and is responsible for up to 30% of all web traffic.

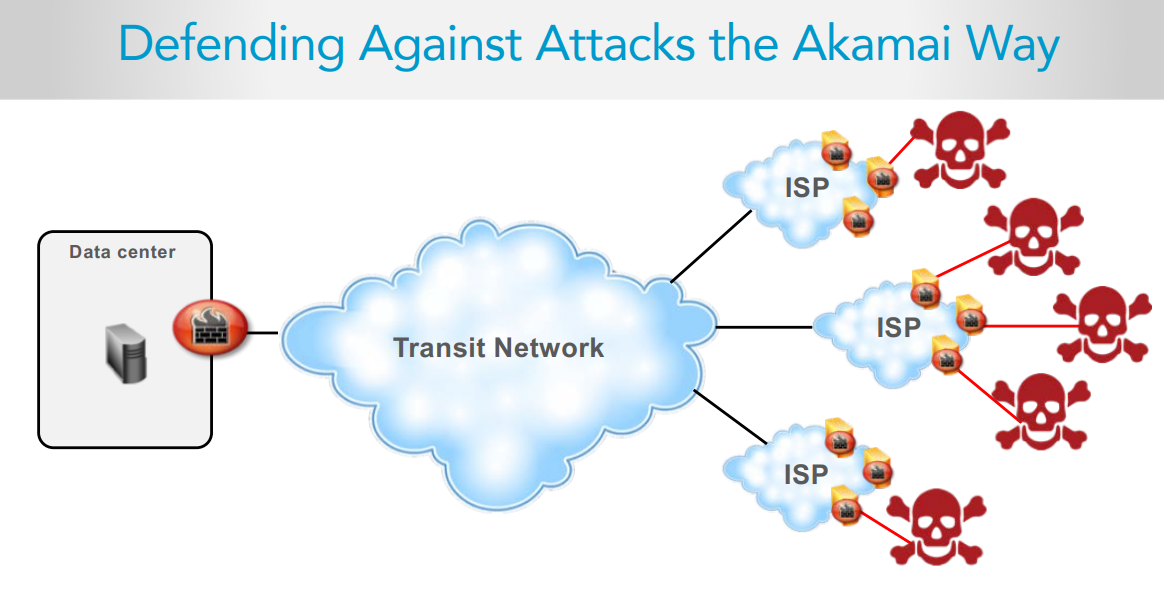

The company is also making a push into the security industry by providing a defensive shield at the ‘edge’ of the CDN as shown in the figure below.

(Source: Akamai 2018 Analyst Day)

Although Akamai has positive free cash flow and earnings (a rarity these days for internet companies), the trailing twelve-month revenue growth of 7.6% is anemic and, in my opinion, there are better investment opportunities out there. Akamai is buying back shares and pushing margins higher as the business erodes through competition and pricing pressure. Akamai doesn’t score well on the Rule of 40 and the stock price is somewhat overvalued. For these reasons, I am giving Akamai a neutral rating.

Business Erosion

While Akamai has the largest global infrastructure, it doesn’t have the highest market share in terms of website count, primarily because they serve mostly large organizations. Akamai is fifth behind Amazon (AMZN) CloudFront, Cloudflare, jsDelivr and Fastly (FSLY).

A big problem for Akamai is that they don’t have a significant economic moat. With the internet shift towards video and large file download, Akamai has been losing business from the internet giants, having determined that they could provide similar services themselves.