Summary

- Acquisitions will hurt gross margin in the short term and also heavily affects valuation.

- Sales and net income growing quickly but not enough to justify stock price.

- Recent share price pullback is because of a return to fundamentals.

Company Overview

Boston Beer, Inc. (SAM) is a top contender in the high end beer manufacturing space and one of the largest craft beer brewers in the U.S. The company was started in 1984 and has seen impressive growth since. It started with the brand Samuel Adams and has since expanded and acquired various brands including: Twisted Tea, Truly Hard Seltzer, Angry Orchard, and most recently, Dogfish Head.

The company’s goal is to be the premier supplier of high end alcoholic beverages. It intends on doing this through leveraging its considerable size as well as increasing its brand visibility and taking advantage of current social trends shifting toward consumers preferring more variety in taste in their alcohols.

Industry Overview

Not much of an introduction is needed for the alcohol industry, but we will give it a shot anyway. The industry was primarily dominated by a few names for many years, most notably very large beer manufacturers. Anheuser-Busch InBev (BUD) and Molson Coors Beverage Company (TAP) controlled 90% of domestic beer production, excluding imports, by 2008. This trend represented the demand for cheap, mass-produced beer.

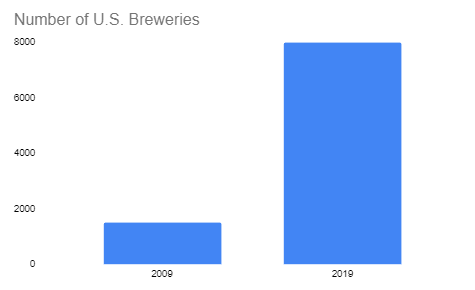

Over the past few years a different trend has emerged. From 2009 to 2019 the number of breweries in the United States has expanded from roughly 1,500 to over 8,000 in 2019. The vast majority of these new breweries are craft breweries. This trend highlights the preference shift from cheap, mass-produced beer to more flavorful beers. Craft beer is also generally more expensive, representing a shift from more frequent cheap beer drinking to less frequent, less price-conscious beer drinking. This shift has seen the two largest beer manufacturers losing U.S. market share from the 90% noted down to 70% over a decade.

Source: My Calculations

Investment Thesis

Boston Beer, Inc. has great beer and other alcoholic beverages as well as strong brand recognition in an industry that has seen growth in demand for craft beers in a short amount of time. These factors have led to too much optimism and forced the stock price to run up too high and unrealistic sales growth would be needed to justify the current price. Between the sales growth needed to justify the current stock price and gross margin suppression in the short-term due to acquisitions, we believe the stock is heavily overvalued.