Summary

- The market overreacted last week to the early-stage clinical program setback, the discontinuation of VX-814 due to toxicity problems.

- However, last week's reaction underscores the need to expand the pipeline.

- Vertex is attractively valued at current levels based on the cystic fibrosis franchise alone, but there is a limit to value creation from the franchise.

- The company will likely use its growing cash balance to address the problem in the following quarters and years.

- I do much more than just articles at Growth Stock Forum: Members get access to model portfolios, regular updates, a chat room, and more. Get started today »

Shares of Vertex (VRTX) declined 20% last week after the company announced the discontinuation of VX-814, the company’s candidate for alpha-1 antitrypsin deficiency. The decline seems disproportionate to the perceived value of this program, but it underscores Vertex’s main weakness - its relatively early-stage and unproven pipeline outside of cystic fibrosis (CF). The stock looks attractively valued today based on growth estimates, but there is a limit to value creation coming from the CF franchise, and the company should be more aggressive with pipeline building in the following quarters and years.

VX-814 was not worth anywhere near $13 billion, but the clinical setback has impacted investor perception of the company’s pipeline

Vertex’s valuation was cut by approximately $13 billion when the company announced the discontinuation of the VX-814 program for alpha-1 antitrypsin deficiency (AATD). The company was running a phase 2 trial to determine the safety and pharmacokinetics of VX-814, and it observed elevated liver enzymes in several patients. In four patients, across different doses, elevations greater than 8 times the upper limit of normal were noted, and the analysis of the PK data indicated that exposures achieved were too low and that it is not feasible to safely reach targeted exposure levels to meaningfully increase AAT levels (AAT is the deficient protein).

But all is not lost in AATD, as Vertex has a second candidate in development, VX-864, which is also in a phase 2, proof-of-concept study. The study was initiated in July 2020, and initial results are expected in 1H 2021.

There is no way to claim this program was valued anywhere near $13 billion (especially considering the lack of positive clinical proof-of-concept data), but the failure underscores the company’s main weakness - its reliance on the CF franchise and the lack of meaningful pipeline behind it.

CF franchise remains the key value driver, and the company should use increasing cash flows to expand the pipeline

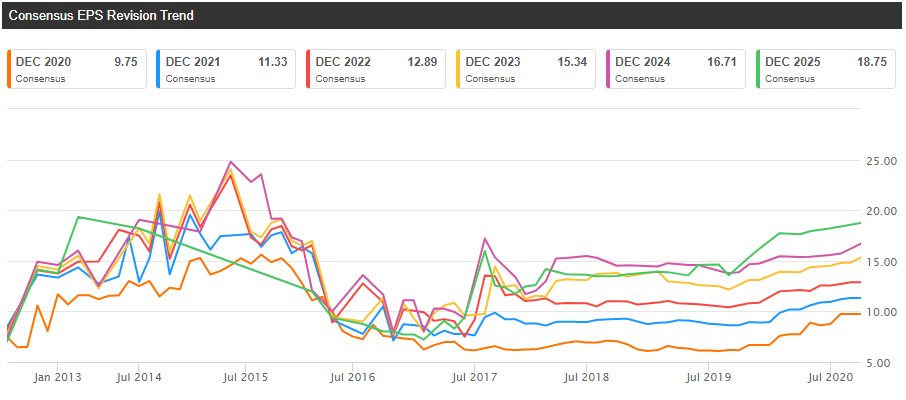

Vertex appears attractively valued based on its CF franchise alone. The stock is trading at approximately 20x next year’s EPS, which seems relatively low for a company delivering 30%+ revenue growth and one in the midst of significant margin expansion and earnings growth. And earnings and revenue revisions keep trending higher, which is what you want to see in a growth stock. As an example, the 2021 EPS consensus was $8.93 at the end of 2019 and it is $11.33 now. Similarly, the revenue consensus increased from $5.73 billion to $6.82 billion.

Source: Seeking Alpha

Estimates are going up due to the strong launch of Trikafta, the first triple combination therapy approved to treat patients with the most common CF mutation. Trikafta was approved in the U.S. in Q4 2019 for patients aged 12 and older, and it has already reached $918 million in net sales in the second quarter of 2020. And it is not even launched in Europe yet (it will be called Kaftrio in Europe). Approval in Europe is expected by year-end, and it should represent a nice tailwind for the company in 2021 and beyond.