Summary

- Corning, an electronics component manufacturer, has a different business model based on induced demand.

- Profitability, which has suffered in the first half of the year, should be back in the second part of the year due to cost-cutting measures.

- Going forward, this diversified company should benefit more as a supplier for COVID vaccine manufacturers and test kits producers.

- There are risks due to the economic downturn but financial position is a strong positive.

- Valuations are on the low side and Corning is a buy.

Corning (GLW) is a diversified company whose performance is often erroneously associated with the whims of the auto and computer industries. This innovative company with a market cap of $24.7 billion is not limited to just these two spheres of the economy.

One of its strengths is Valor technology it developed back in 2017.

Today, this technology has significant potential to save lives in context of the fight against COVID as I will further explain.

In addition, while having suffered from some setbacks in the enterprise and carrier businesses, it is active in optics and networking products which are key ingredients needed to build 5G networks.

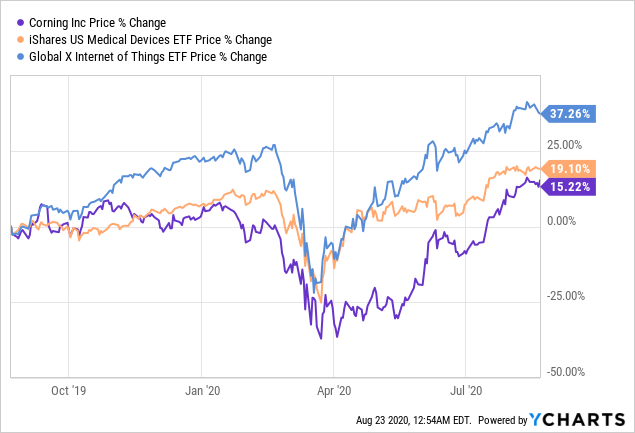

Figure 1: Comparing Corning with the iShares U.S. Medical Devices ETF (IHI) and the Global X Internet of Things Thematic ETF (SNSR).

Data by

Data byI also evaluate how the setbacks are being addressed so that they do not result in longer-term pain going forward and provide an indicative stock price for those willing to position themselves.

To start with, it is important to provide investors with insights as to Corning's particular business model and specifically how it relates to profitability.