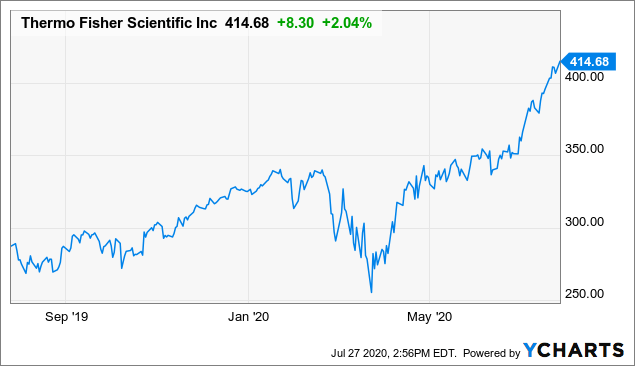

- Thermo Fisher's share price has increased by more than 60% since the March lows.

- Despite a good free cash flow result in H1, the valuation is perhaps getting a bit ahead of itself.

- Trading at a current free cash flow yield of around 3%, I am not chasing the stock here but am hoping for a strong pullback.

- Looking for a portfolio of ideas like this one? Members of European Small-Cap Ideas get exclusive access to our model portfolio. Get started today »

Introduction

Since my previous article on Thermo Fisher (TMO) in February, the company’s share price was only mildly impacted by the COVID-19 outbreak, and I never had the chance to initiate a long position at bargain prices. At this point, the company is already trading again at about 65% above its March lows, and I wanted to check if this share price surge is sustainable from a fundamental perspective.

Data by YCharts

Data by YChartsA strong operating cash flow leads to a substantial amount of free cash flow

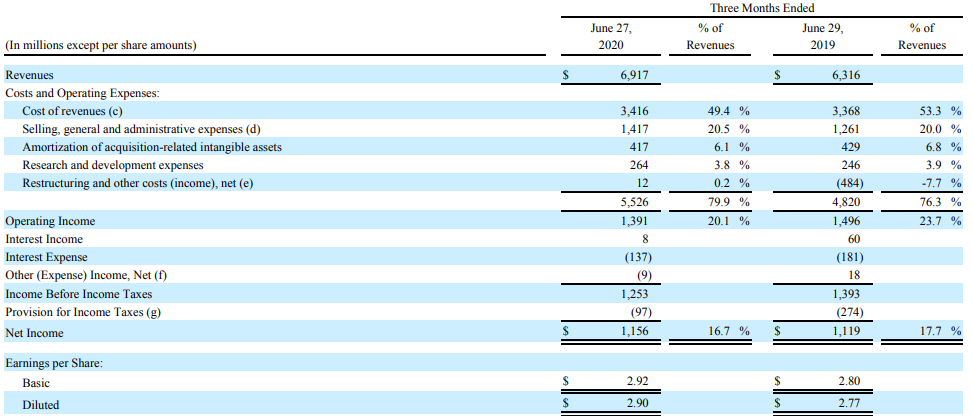

Looking at the recently published financial results, Thermo Fisher had a very strong second quarter as its revenue increased by 10% while the adjusted EPS was boosted to almost $4/share (the adjustment is predominantly related to the amortization of the acquisition-related intangible assets). The strong revenue increase was predominantly caused by a $1.3B revenue boost related to COVID-19. While that’s great, this also means the non-COVID related revenue was also hit, in line with the expectations.

During the second quarter, the revenue indeed did increase to $6.92B, but as you can see in the image below, the operating margin decreased from 23.7% to 20.1%. That sounds problematic, but this is actually entirely caused by a small restructuring expense of $12M compared to a $484M gain recorded in Q2 last year. Excluding that one-time gain in 2019, the operating margin would have been just over 16%. So although the quarterly income statement of Thermo doesn’t look too fantastic compared to Q2 2019, keep in mind the non-recurring items had a huge impact in 2019.

Source: financial statements

Looking at the EPS in the first semester ($4.91/share reported, $6.83/share on an adjusted basis), Thermo Fisher appears to be a little bit ahead of itself considering it is trading at in excess of 25 times its annualized adjusted net income at the current levels.

That being said, I realize there are some substantial non-cash items mentioned in the income statement, and the free cash flow result should be substantially higher than the reported net income and perhaps also higher than the adjusted net income.