Summary

- HubSpot is the World leader in inbound marketing.

- The company has been successful in adding new services and cross-selling them to existing customers.

- HubSpot operates as a "platform", which makes its business model extremely light and easily scalable.

- Valuation is reasonable given the strong top-line growth, increasing EBITDA and safe Balance Sheet.

Company Overview

Ticker: (HUBS)

Sector: Information Technology

Market Cap: $9.7bn

LTM Cash/Debt: $968.6m / 610.5m

1Y Return: 32.45%

EV/Revenue: 13.1x

52-Week Range: $90.84 - $231.17 ($225.04 at the time of writing)

HubSpot (HUBS) is the World leader in inbound marketing, the strategy according to which companies don't actively seek customers (for instance through emails or cold calls) but they let the quality of their content bring customers to them. This new marketing philosophy is why HubSpot has brought in thousands of new customers and grew its top line at an impressive rate.

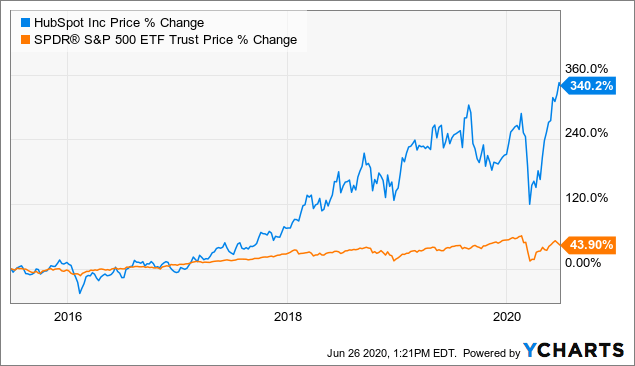

5-year performance as of June 27th, 2020

But what makes inbound marketing so special? The strategy drastically improves customer experience and, at the same time, is a much more effective way of building trust by offering customers information they really value. In simpler terms, inbound marketing is a more sustainable marketing strategy than outbound marketing (which refers to pushing a product to a customer through various marketing channels).

Since 2012, HubSpot has been extremely successful in capitalizing on this opportunity, growing its top-line at an impressive 40%+ CAGR over the last 5 years.

Source: HubSpot

The company climbed 18.6% in May thanks to better that expected first quarter results on May 6, with revenue increasing 31% YoY to reach $199m (vs $190.9m estimates). Most of the revenue is coming from its subscription-based model: subscription revenue reached $191.2m, representing a 33% YoY increase, while total customers were up 30% to hit 78,776.