Summary

- CVS Health reported solid third-quarter results with Health Care Benefits even outperforming expectations with the retail pharmacy segment meeting expectations.

- Especially the CVS MinuteClinic, the HealthHUB and the benefit of having a “CVS Pharmacy near me” will be an advantage for the company going forward.

- The company’s market-leading position and the demographic shift will increase the demand for different healthcare products and services.

- CVS is not only paying a healthy dividend, but the stock is still deeply undervalued, making it a great investment.

- Looking for a helping hand in the market? Members of Moats & Long-Term Investing get exclusive ideas and guidance to navigate any climate. Get started today »

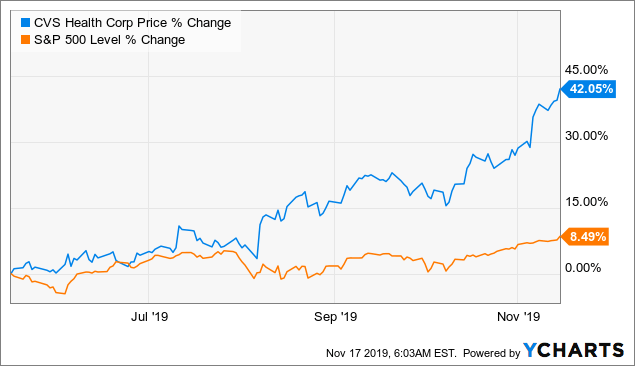

In 2019, I already published two very bullish articles on CVS Health Care (CVS) - one in March 2019 and one in July. Since my last article, the total return of CVS was 37.6% (including dividends), compared to the S&P 500 (SPY) which could return only 6% in the same time frame.

Data by YCharts

Data by YChartsA few days ago, CVS reported third-quarter results, and I am still very bullish on the company. In the following article, I will look at the last quarterly results, discuss management’s strategy a little bit and describe once again why CVS is a great long-term investment. But we will also look at the risks surrounding the company and its balance sheet, before we end with an intrinsic value calculation.

Quarterly Results

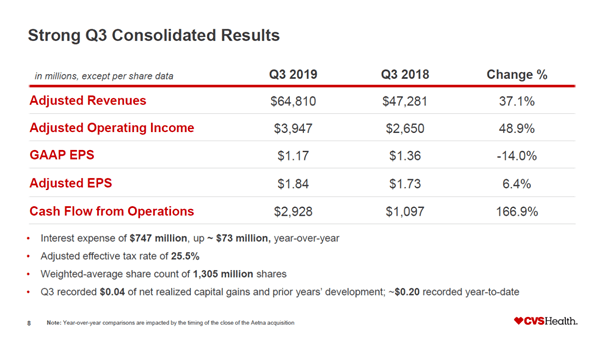

CVS was able to report good third-quarter results. Revenue increased 37.1% compared to the same quarter last year, but the high growth rate is the result of the company’s acquisition of Aetna last fall. While GAAP EPS decreased 14% and was only $1.17, adjusted EPS increased 6.4% to $1.84 (even 5 cent above the higher end of the guidance range). I am certainly not a big fan of adjusted, non-GAAP numbers, and when using it, we should at least know how the company is calculating its adjusted EPS numbers. Among the non-GAAP adjustments management made, we have to point out the amortization of intangible assets (increasing EPS $0.46) and the loss on divestiture of subsidiary (increased EPS $0.16). You have to decide for yourself if these adjustments make sense or not. Instead, we can also focus on the cash flow from operations, which is much harder to “fake” and increased 167% in the third quarter to $2,926 million.

(Source: CVS Q3 Investor Presentation)

The company saw strong revenue and script growth, which was outpacing the marketplace and driving 110 basis point increase in retail script share to 26.6%. It also reduced the net debt by $2.9 billion in the third quarter and paid off $1.5 billion term loan and $850 million in maturities. For the full year of 2019, CVS expects that $4.7-5.1 billion will be available for debt repayment.

When looking at the different segments, performance was especially driven by strong operating execution across the enterprise, with Health Care Benefits exceeding expectations (Retail/LTC and Pharmacy Service performed in line with expectations).